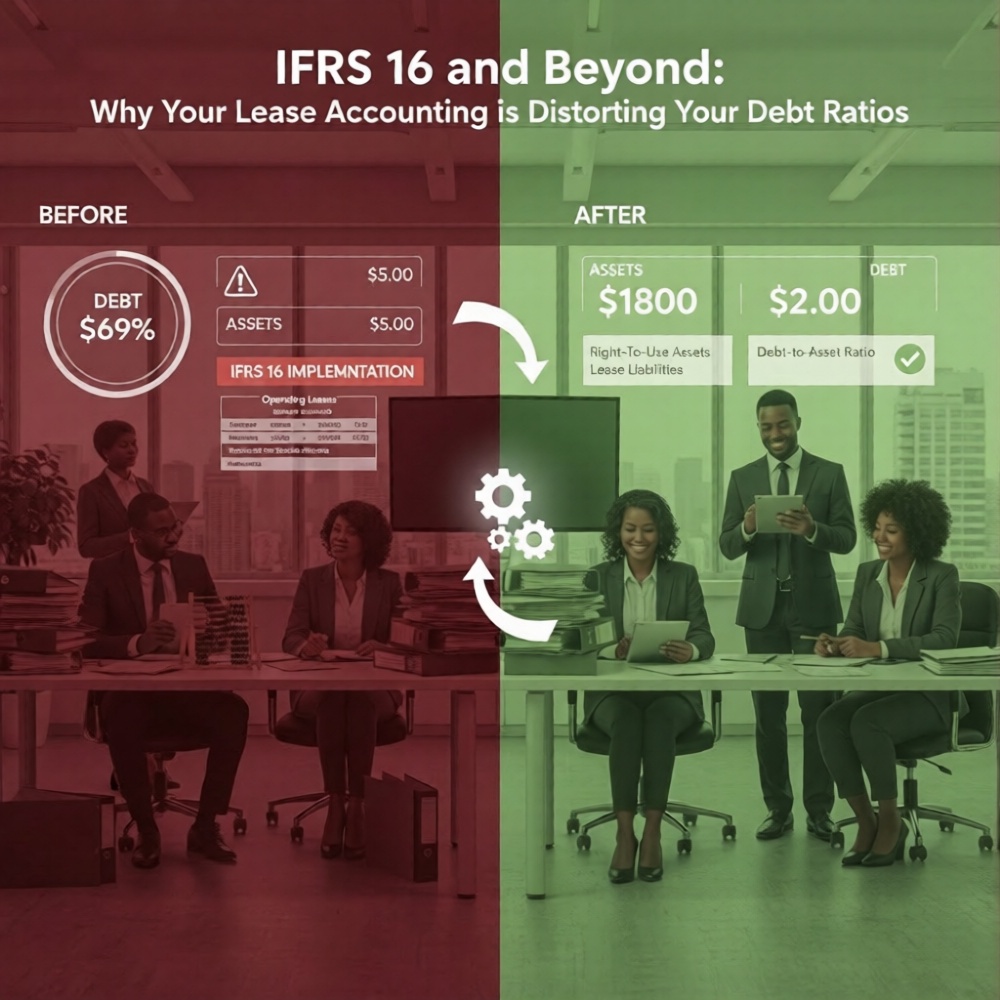

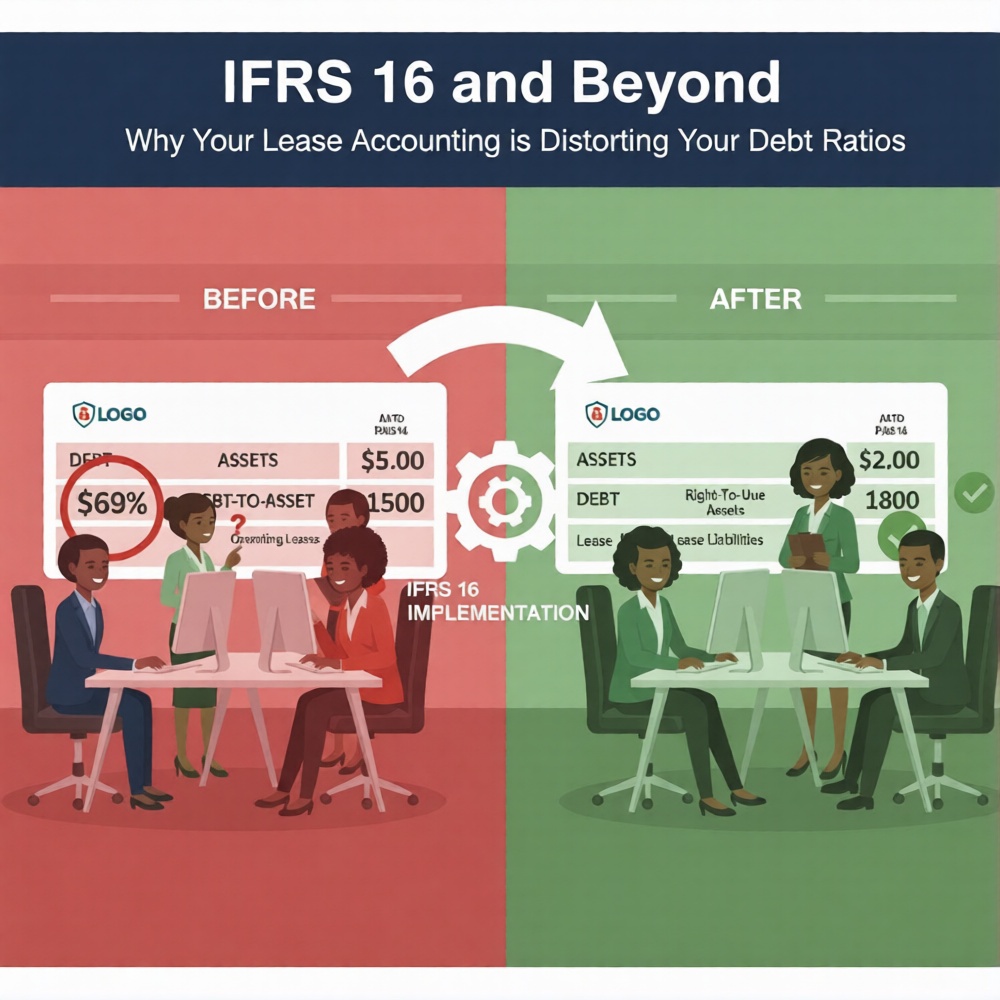

- Since IFRS 16, almost all leases must appear on the balance sheet as a right-of-use (ROU) asset and a matching lease liability, removing the old off-balance-sheet treatment for lessees.

- Capitalizing leases increases reported liabilities and assets, pushing up debt-to-equity and leverage ratios that lenders use for covenant compliance.

- Common mistakes include ignoring short-term and low-value leases, using incorrect discount rates, misclassifying assets, and neglecting IFRS 16 disclosure requirements.

- Kenyan tax treatment can differ from accounting treatment, creating deferred tax assets or liabilities, and eTIMS validation of leased asset invoices supports deductibility.

- Accurate, automated lease accounting protects creditworthiness, prevents covenant breaches, and builds investor confidence by reflecting the company's true economic position.

Leases are no longer off-balance-sheet items. Since the adoption of IFRS 16, companies in Kenya must recognize most leases on their balance sheets, affecting debt ratios, covenants, and financing decisions. Yet, many businesses still treat leases as simple rental expenses, unintentionally distorting their financial metrics and misrepresenting financial health to investors, lenders, and auditors.

For CFOs, finance managers, and business owners, understanding the implications of IFRS 16—and planning for accurate lease accounting—is critical for creditworthiness, capital raising, and compliance in 2026.

At Adamjee Auditors, a member of SFAI Global, we guide Kenyan businesses through lease accounting, IFRS compliance, and strategic financial reporting to ensure debt ratios reflect the true economic position of your company.

What Is IFRS 16 and Why It Matters

IFRS 16, effective for annual reporting periods starting on or after January 1, 2019, fundamentally changed lease accounting. Key requirements include:

-

Recognition of a right-of-use (ROU) asset and corresponding lease liability on the balance sheet for almost all leases.

-

Front-loaded interest and depreciation expenses for finance leases, altering profit and loss reporting.

-

Distinction between operating and finance leases largely removed for lessees.

For businesses still following old “off-balance-sheet” approaches, debt ratios—like debt-to-equity and leverage ratios—may be understated, affecting:

-

Bank covenant compliance

-

Loan approval

-

Investor perception

-

Risk assessment

Our Audit and Assurance Services help verify IFRS 16 compliance and correct balance sheet presentation.

How Lease Accounting Distorts Debt Ratios

Debt ratios are sensitive to liabilities. Under IFRS 16:

-

Lease liabilities increase reported debt.

-

Previously “rental” expenses are now capitalized, increasing total assets and depreciation.

-

Short-term and low-value leases are treated differently, but many companies misclassify them.

| Metric | Pre-IFRS 16 | Post-IFRS 16 Misapplied | Correct IFRS 16 |

|---|---|---|---|

| Total Liabilities | 50,000,000 | 50,000,000 | 75,000,000 |

| Right-of-Use Assets | 0 | 0 | 75,000,000 |

| Debt-to-Equity | 1.0x | 1.0x | 1.5x |

| EBITDA | 20,000,000 | 20,000,000 | 23,500,000 |

Misapplied accounting creates the illusion of lower leverage, potentially violating covenants once properly accounted for.

For strategic insights, explore our CFO Advisory Services.

Common IFRS 16 Implementation Mistakes

-

Ignoring short-term or low-value leases: Even small leases can accumulate into material amounts.

-

Incorrect discount rates: Lease liabilities must be discounted using the appropriate incremental borrowing rate.

-

Improper asset classification: Right-of-use assets must be reconciled with finance and operating lease classifications.

-

Failure to update contracts regularly: Lease modifications must be accounted for promptly.

-

Neglecting disclosure requirements: IFRS 16 requires detailed notes in financial statements, including maturity analysis, interest expense, and cash flows.

Our Bookkeeping Services and Tax Compliance Services ensure accurate lease accounting and disclosure compliance.

IFRS 16 and Loan Covenants

Many lenders in Kenya now include leverage ratios and EBITDA covenants in loan agreements. Misstating lease liabilities can lead to:

-

IFRS 16 brings lease liabilities onto the balance sheet—misstated leases can distort debt ratios, risk covenants, and mislead investors. Covenant breaches

-

Higher interest charges

-

Repricing or withdrawal of credit lines

-

Reduced investor confidence

Accurate reporting ensures financial stability and preserves borrowing capacity.

We support businesses in evaluating loan agreements and recalculating ratios under IFRS 16 through our Audit and Assurance Services.

Lease Accounting Automation: A 2026 Necessity

Manual tracking of lease contracts, payments, and amortization schedules is increasingly risky. Automation helps:

-

Centralize lease data

-

Apply correct discount rates automatically

-

Generate ROU asset schedules and lease liability reconciliations

-

Integrate with ERP and accounting systems

-

Maintain audit-ready records

Our Offshore Accounting Services can integrate automated lease accounting with broader financial processes for cost-efficient compliance.

Tax Implications of IFRS 16

While IFRS 16 governs accounting, tax treatment may differ. In Kenya:

-

Lease payments for tax purposes may still be deductible over time

-

Differences between accounting depreciation and tax treatment can create deferred tax assets or liabilities

-

eTIMS validation of leased asset invoices ensures deductibility

Our Tax Compliance Advisory Services reconcile tax treatment with IFRS reporting to minimize unexpected exposures.

Investor Perception: Transparency Builds Confidence

Investors scrutinize debt ratios and leverage when evaluating creditworthiness. Misstated leases can:

-

Overstate EBITDA

-

Understate debt

-

Distort return on assets and equity

Transparent, IFRS-compliant lease accounting signals financial discipline and enhances investor confidence.

Learn more About Adamjee Auditors and our advisory approach to financial reporting.

Preparing for IFRS 16 Audits

Key steps for audit readiness include:

-

Inventory all lease contracts

-

Identify and classify short-term, low-value, and finance leases

-

Calculate ROU assets and lease liabilities accurately

-

Document all assumptions and discount rates

-

Integrate lease schedules with the general ledger and financial reporting systems

Our Statutory Audit Kenya Guide provides a roadmap for IFRS 16 audit readiness.

IFRS 16 transforms lease obligations from hidden off-balance-sheet items into transparent financial liabilities. Misalignment distorts debt ratios, risks covenant breaches, and can mislead investors.

Adamjee Auditors combines:

-

Local regulatory expertise

-

IFRS-compliant lease accounting solutions

-

Audit readiness and assurance

-

Global insight through SFAI Global

Proper lease accounting is not just compliance—it is strategic financial management.