- Payroll is now a regulated financial function; errors trigger penalties, arrears, and multi-year payroll tax audits.

- Common Housing Levy errors include applying the levy to non-qualifying income, omitting the employer contribution, and late remittances.

- NSSF Tier II contributions must be calculated correctly above the lower earnings limit with Tier I and Tier II portions properly separated.

- PAYE errors often arise from misclassifying housing benefits, allowances, and benefits in kind as non-taxable.

- Spreadsheet-based payroll is very high risk; cloud payroll with updated statutory tables and audit trails reduces exposure.

Statutory Payroll Compliance has become a high-risk area for Kenyan employers as labor regulations, statutory deductions, and reporting requirements grow more complex. Miscalculations in payroll no longer result in minor adjustments — they now trigger penalties, back-pay obligations, and formal payroll tax audit reviews.

Employers must treat payroll as a regulated financial function rather than an administrative task.

Why Statutory Payroll Compliance Is Under Increased Scrutiny

Kenyan regulatory authorities have intensified oversight of payroll processes due to changes in employment law, social security reforms, and digital tax enforcement systems.

Key drivers include:

-

Expanded Housing Levy compliance Kenya requirements

-

Revised NSSF Tier II contributions structures

-

Greater cross-matching of PAYE data with tax filings

-

Increased labor inspections

Adamjee Advisory Insight 2026:

Payroll errors are now commonly identified through automated reconciliation systems. Discrepancies between declared payroll and remittances are flagged faster than in previous years.

Professional payroll service oversight reduces exposure to regulatory queries.

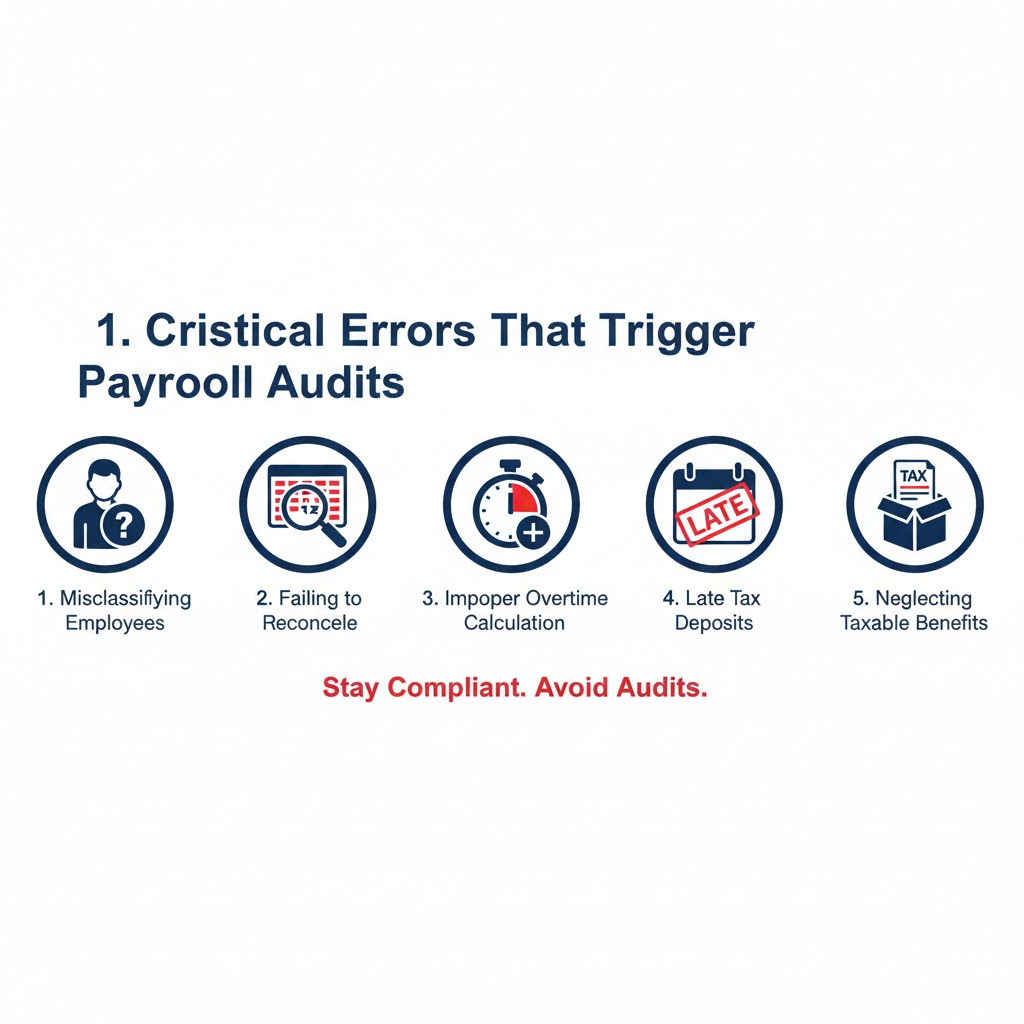

1. Incorrect Housing Levy Calculations

Housing Levy compliance Kenya requirements continue to create confusion for employers regarding deduction bases, employer contributions, and reporting.

Common errors include:

-

Applying the levy to non-qualifying income

-

Failing to include employer contribution portion

-

Delayed remittances

-

Inconsistent payroll system configurations

| Error Type | Compliance Impact | Risk Level |

|---|---|---|

| Under-deduction | Employer liability for arrears | High |

| Over-deduction | Employee disputes | Medium |

| Late remittance | Penalties and interest | High |

| Reporting mismatch | Payroll tax audit trigger | High |

2. Misapplication of NSSF Tier II Contributions

NSSF Tier II contributions require correct calculation above the lower earnings limit and proper fund allocation.

Frequent compliance issues:

-

Incorrect upper earnings limit application

-

Failure to separate Tier I and Tier II portions

-

Incorrect remittance to approved pension schemes

-

System misconfigurations during payroll processing

Adamjee Advisory Insight 2026:

Employers transitioning payroll systems or scaling staff numbers often misapply contribution thresholds, increasing audit exposure.

3. PAYE Errors Due to Allowance Misclassification

PAYE discrepancies arise when allowances and benefits are incorrectly treated as non-taxable.

Problem areas include:

-

Housing allowances

-

Overtime payments

-

Non-cash benefits

-

Travel allowances without supporting policy

| Item | Common Mistake | Result |

|---|---|---|

| Housing benefit | Treated as exempt | PAYE underpayment |

| Allowances | Not aggregated | Tax under-deduction |

| Benefits in kind | Omitted | Audit reassessment |

These issues frequently trigger payroll tax audit adjustments.

4. Inadequate Payroll Documentation

Payroll compliance extends beyond calculations. Documentation must support every deduction.

Required records include:

-

Employment contracts

-

Payroll registers

-

Deduction schedules

-

Remittance confirmations

-

Employee tax cards

Lack of documentation shifts the burden of proof to the employer.

Adamjee Advisory Insight 2026:

Digital payroll systems with structured audit trails reduce documentation risk and support compliance during inspections.

5. System Errors in Payroll Processing

Manual or outdated payroll systems increase compliance risk.

System weaknesses include:

-

Spreadsheet-based payroll

-

Lack of automated tax tables

-

Incorrect statutory updates

-

Absence of segregation of duties

| System Type | Compliance Risk |

|---|---|

| Excel payroll | Very high |

| Legacy software | High |

| Cloud payroll with updates | Low |

Professional payroll service providers maintain updated statutory configurations.

2026 Regulatory Risk Factors

Statutory Payroll Compliance now intersects with broader compliance frameworks:

-

Digital reconciliation of tax remittances

-

Increased employer audits

-

Expanded statutory levies

-

Stricter employment record verification

Errors in one levy often lead to a full payroll tax audit covering multiple years.

When Should You Conduct a Payroll Compliance Audit?

You should initiate a payroll compliance audit if:

-

Staff numbers increased significantly

-

Payroll software changed

-

Regulatory updates were recently introduced

-

Historical payroll errors were discovered

-

Employee disputes have arisen

Early detection reduces penalties and reputational damage.

Benefits of Professional Payroll Oversight

A structured payroll service provides:

-

Accurate statutory deductions

-

Timely remittances

-

Audit-ready documentation

-

Updated tax tables

-

Reduced compliance exposure

Payroll should be treated as a compliance system, not just a payment process.

Common Payroll Compliance Red Flags

| Red Flag | Why It Matters |

|---|---|

| Manual payroll adjustments | Increased error risk |

| Inconsistent payslips | Possible deduction errors |

| Unreconciled statutory balances | Audit trigger |

| Staff complaints | Early warning sign |

| No periodic payroll review | Hidden long-term risk |

Strategic Outlook

Statutory Payroll Compliance is becoming one of the most scrutinized operational areas for Kenyan businesses. The cost of payroll errors now exceeds the cost of professional oversight.

Organizations that proactively conduct payroll audits reduce risk exposure and maintain workforce trust.

Executive Summary

Statutory Payroll Compliance failures often stem from system weaknesses, misunderstanding of levy rules, and documentation gaps. Housing Levy compliance Kenya and NSSF Tier II contributions are high-risk areas that demand structured payroll tax audit readiness.

Proactive payroll audits prevent penalties, employee disputes, and regulatory enforcement actions.

Gain Clarity and Confidence in Your Finances

Navigate the complexities of compliance, tax, and financial management with a trusted partner. Adamjee Auditors, a member of Santa Fe Associates International (SFAI), provides audit, tax, and advisory services to help your business achieve its goals.

Schedule a consultation with our expert team in Nairobi or Mombasa to discuss your business needs.

Nairobi Office

Park View Heights, Mombasa Road, OR Mbandu Complex, Langata Road

+254 717 908 241

info@adamjeeauditors.com

Mombasa Office

Suite 401, Motorwalla Building, Jomo Kenyatta Road

+254 703 899 606 / +254 717 908 241

info@adamjeeauditors.com

https://adamjeeauditors.com/