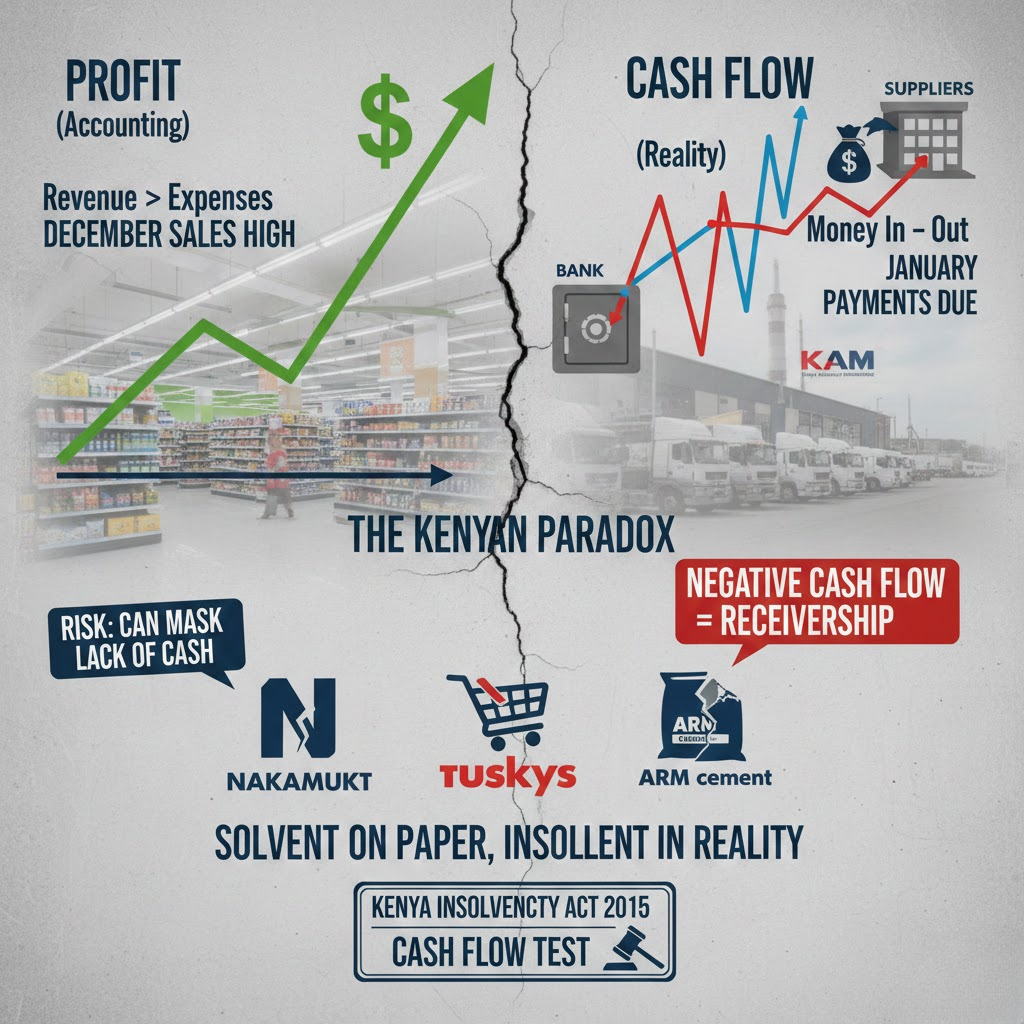

- Profit is revenue minus expenses over a period, while cash flow is the actual movement of money; a company can be profitable yet insolvent if cash is locked in unpaid invoices, inventory, or other assets.

- Common causes of cash flow shortages include delayed receivables (especially from government contracts), high inventory levels, unexpected expenses, and heavy debt obligations.

- From 2026, KRA disallows deductions for expenses not supported by eTIMS invoices, raising tax liabilities that can strain cash flow even when profitability stays strong.

- Practical fixes include real-time cash flow tracking, negotiating shorter customer payment terms, maintaining a cash reserve, and using invoice financing for temporary gaps.

- Leaders should review monthly cash flow statements alongside profit and loss reports and forecast cash needs at least 12 months ahead, including regulatory obligations.

Cash Flow vs. Profit: Why Solvent Kenyan Companies Still Go into Receivership

Understanding Cash Flow and Profit

Profit reflects a company’s accounting performance over a period, calculated as revenue minus expenses. Cash flow tracks the actual movement of money in and out of a business. While profit can look healthy on paper, cash flow measures liquidity—the ability to pay suppliers, employees, and creditors. A company can be profitable yet insolvent if cash is tied up in unpaid invoices, inventory, or other assets.

In Kenya, SMEs often face delayed client payments, especially from government contracts. Even profitable companies can experience liquidity shortages that trigger financial distress. Understanding the difference between profit and cash flow is essential for CEOs and CFOs who want to avoid sudden insolvency.

Common Causes of Cash Flow Shortages

Several factors can cause a profitable Kenyan business to experience cash flow problems:

-

Delayed Receivables: Customers or government agencies paying late can restrict liquidity.

-

High Inventory Levels: Overstocking ties up cash that could cover operating expenses.

-

Unexpected Expenses: Regulatory fines, tax adjustments, or equipment repairs can create sudden cash gaps.

-

Debt Obligations: Servicing loans without adequate cash inflows can lead to insolvency.

For example, a Nairobi-based manufacturing firm recorded profits for three consecutive years but faced delayed government payments. Its inability to cover payroll and supplier obligations eventually forced it into receivership. Businesses can learn from these cases and proactively manage cash by monitoring liquidity rather than focusing solely on profit.

The Impact of 2026 KRA Regulations on Cash Flow

Kenya Revenue Authority’s (KRA) 2026 updates significantly affect liquidity management. Expenses not supported by eTIMS invoices are now disallowed, meaning companies cannot claim deductions for such expenditures. Firms that fail to comply face higher tax liabilities, which can strain cash flow even if profitability remains strong.

Additionally, the KRA Automated Payment Plan (APP) offers structured relief for taxpayers but requires careful planning. Businesses that neglect cash flow projections while assuming profits cover all obligations risk falling behind on payments. Adamjee Auditors provides guidance through tax compliance advisory to help Kenyan companies navigate these regulatory changes and maintain liquidity.

Case Examples of Solvent Companies Entering Receivership

Several Kenyan companies have demonstrated that solvency on paper does not guarantee survival:

-

Company A – Manufacturing: Despite positive profits, delayed payments from government contracts led to insufficient cash for day-to-day operations.

-

Company B – Construction: Aggressive project expansion and overstocked materials caused a temporary liquidity crunch.

-

Company C – Retail: High seasonal sales led to profits, but poor management of accounts payable created cash flow gaps, resulting in receivership proceedings.

These cases illustrate the importance of reconciling profit with actual cash availability. Monitoring cash flow statements alongside profit and loss accounts is critical for decision-making.

Tools and Strategies to Improve Cash Flow

Kenyan companies can adopt several strategies to avoid insolvency despite being profitable:

-

Implement real-time cash flow tracking using modern accounting software. Adamjee Auditors can guide businesses in choosing the right accounting software.

-

Negotiate shorter payment terms with customers and extend terms with suppliers where feasible.

-

Maintain a cash reserve to cover unexpected expenses or regulatory payments.

-

Consider invoice financing or structured credit facilities to manage temporary liquidity gaps.

These strategies, when applied consistently, reduce the risk of receivership caused by short-term cash flow shortages.

Leveraging Professional Advisory Services

Partnering with experienced auditors and financial advisors ensures businesses remain compliant and financially resilient. Adamjee Auditors, a member of the SFAI Global network, provides audit and assurance services and CFO advisory services to help Kenyan companies manage cash flow, adhere to KRA regulations, and maintain profitability while avoiding insolvency.

In addition, offshore accounting services can improve cash management for companies with cross-border operations, ensuring timely reporting and regulatory compliance. Learn more about why your business may need offshore accounting.

Monitoring Cash Flow for Long-Term Stability

Sustained profitability requires disciplined cash flow management. Kenyan business leaders should:

-

Review monthly cash flow statements alongside profit and loss reports.

-

Forecast cash needs for at least 12 months, factoring in regulatory obligations such as eTIMS compliance.

-

Maintain contingency plans for tax liabilities or unexpected operational costs.

Proactive cash flow monitoring helps prevent situations where a company appears solvent but faces operational insolvency, ultimately protecting investors, employees, and business continuity.

Gain Clarity and Confidence in Your Finances

Navigate the complexities of compliance, tax, and financial management with a trusted partner. Adamjee Auditors, a member of Santa Fe Associates International (SFAI), provides world-class audit, tax, and advisory services to help your business achieve its goals.

Schedule a consultation with our expert team in Nairobi or Mombasa to discuss your business needs.

Nairobi Office

Park View Heights, Mombasa Road, OR Mbandu Complex, Langata Road

Phone: +254 717 908 241

Email: info@adamjeeauditors.com

Mombasa Office

Suite 401, Motorwalla Building, Jomo Kenyatta Road

Phone: +254 703 899 606 / +254 717 908 241

Email: info@adamjeeauditors.com

Website: https://adamjeeauditors.com/